SMM June 20 News:

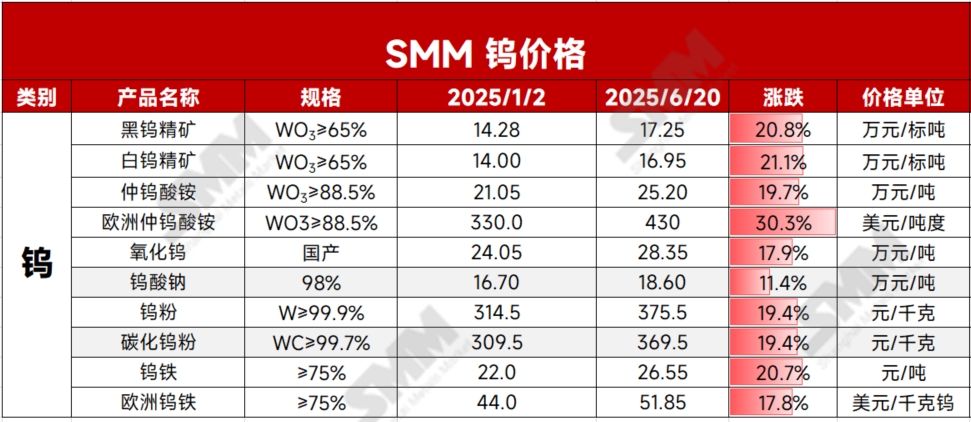

On June 20, major domestic tungsten enterprises successively finalised long-term contract prices for tungsten concentrate and APT products. Among them, the long-term contract price for standard-grade black tungsten concentrate was locked at a high range of 171,000-172,000 yuan per standard mt, while the APT long-term contract price was anchored at 251,000 yuan per mt. The implementation of high-price long-term contracts by major producers has reinforced the "fluctuate at highs" support for the tungsten market in late June, with market trends becoming clearer and prices maintaining a hover at highs pattern in the short term. Looking back at H1 2025, the global tungsten market experienced multiple drivers including policy adjustments, demand surges, and geopolitical competition, leading to a fluctuate upward trend in industry chain prices, with Q2 seeing accelerated highs. Prices of core products such as tungsten concentrate and ammonium paratungstate (APT) repeatedly hit historical records. As of June 20, domestic 65% black tungsten concentrate closed at 172,500 yuan per standard mt, up 20.8% from the beginning of the year, while APT closed at 252,000 yuan per mt, a 19.7% increase YoY. Other tungsten intermediate products and downstream products followed suit, with gains generally ranging between 19%-21%. The overseas market was more significantly impacted by China's export controls. Starting from February 2025, China's tungsten export restrictions triggered supply chain disruptions abroad, causing European APT prices to surge rapidly. By June 18, European APT prices reached $430 per mtu, up 30.3% from the beginning of the year, while European ferrotungsten closed at $51.85 per kg W, a 17.8% increase since early 2025.

First, tightening domestic supply dominates global tungsten industry chain price trends.

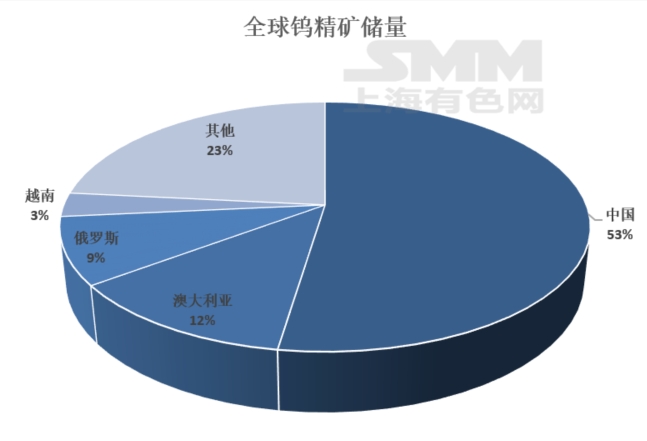

According to USGS data, global tungsten ore reserves stood at 4.6 million mt in metal content as of 2024, with China accounting for 2.4 million mt (52% of global reserves), holding an absolute dominant position in the global tungsten market. Other major tungsten resource locations include Australia (12%), Russia (9%), and Vietnam (3%). As a strategic mineral for China, tungsten resource development is subject to comprehensive policy regulation, covering industry access, total output control, export restrictions, and tax guidance. In 1991, tungsten was officially designated as a state-protected specific mineral by the State Council. Since 2000, total output control measures and the export quota system implemented in February 2025 under the stimulus policy package have limited incremental domestic tungsten mine development, with market supply relying mainly on existing projects, leading to a more stable industry structure.

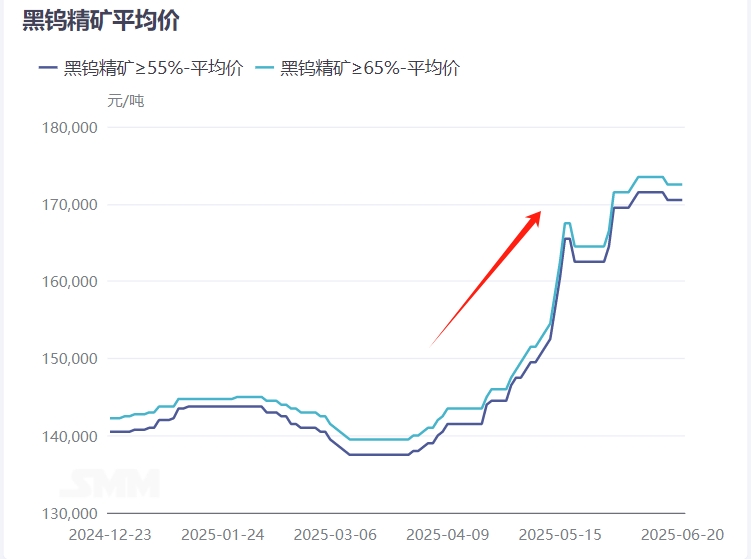

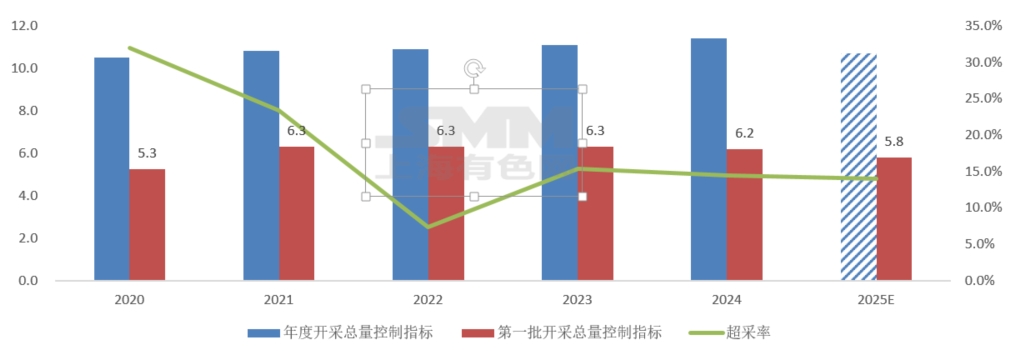

After 2020, with deepening policy adjustments, China's tungsten concentrate over-mining rate narrowed significantly. Data shows that domestic tungsten concentrate production in 2024 was approximately 130,000 mt, with an over-mining rate of around 14%, down 18 percentage points from 2020. On April 21, 2025, the Ministry of Natural Resources issued the first batch of tungsten mining quotas for 2025 at 58,000 mt, down 6.5% YoY, marking the second consecutive year of tightening initial quotas. Based on calculations of a proportional decline, the tungsten concentrate mining quota for the entire year of 2025 is expected to be around 107,000 mt. If the over-mining rate remains at approximately 14%, the annual tungsten concentrate production may only reach 122,000 mt. However, the issue of declining ore grades may exacerbate the shortage of tungsten concentrate. The market has expressed concerns about the future supply of tungsten concentrate, driving up its prices rapidly. By the end of May, the third round and fourth batch of environmental protection checks were fully launched in China, with environmental protection policies remaining stringent, further pushing up ore prices.

Secondly, the release of new overseas tungsten concentrate is slow, and the downstream industry chain for overseas tungsten smelting is incomplete.

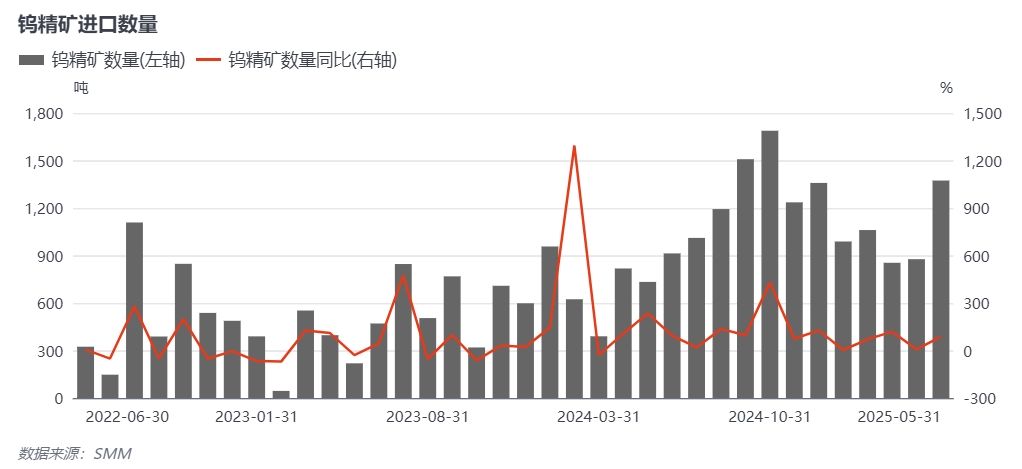

The main contributors to the increase in overseas tungsten concentrate in 2025 are new tungsten mine projects in South Korea and Kazakhstan. Among them, the Sangdong Tungsten Mine in South Korea is planned to commence production in the second half of 2025, with an annual output of 2,300 mt (calculated based on tungsten trioxide) after the first phase reaches full production. The Boguty (Bakuta Tungsten Mine) project in Kazakhstan was completed and put into operation at the end of 2024. After reaching full production, it is expected to process 3.3 million mt of tungsten ore annually, with an estimated output of 5,000 standard mt of tungsten concentrate in 2025. Changes in other new mine projects are relatively small. Additionally, the overseas tungsten smelting sector is underdeveloped, making it difficult for many countries and regions to process tungsten concentrate into other tungsten products even if they have it. This has also led to lower overseas ore prices compared to domestic prices, creating an import window for domestic tungsten concentrate. China is a major producer of tungsten concentrate and also a major importer of overseas tungsten concentrate. From January to May 2025, the total domestic import volume of tungsten concentrate reached 5,153 mt, up 46.3% YoY.

Stable downstream demand and geopolitical instability overseas stimulate strategic stockpiling of tungsten.

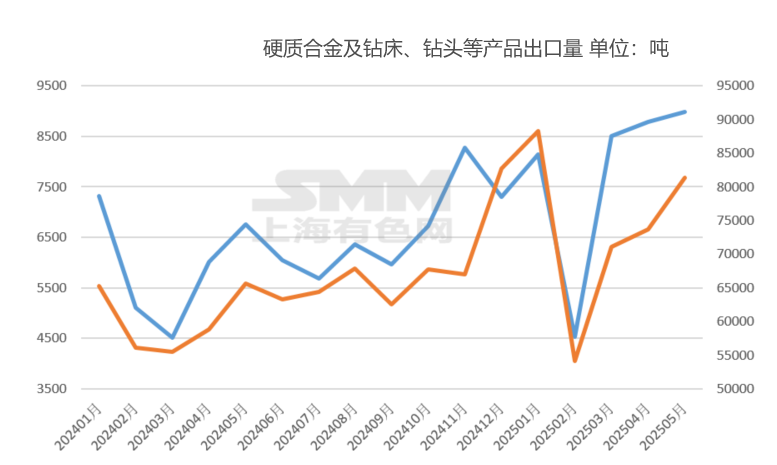

Since the first half of 2025, domestic downstream demand for tungsten in the terminal market has been stable, with the high-end manufacturing sector providing growth points. Among them, the demand for tungsten in humanoid robots and cutting machines has grown steadily, while traditional sectors such as PV tungsten wires have shown mediocre performance. In addition, since the implementation of export controls on domestic tungsten products in February, the exports of domestic tungsten intermediate products have declined significantly, but the exports of terminal tungsten products have increased notably, enhancing the added value of domestic tungsten industry chain exports. Taking cemented carbide and drill bit and drilling machine products as examples, according to customs data, the total export volume of domestic cemented carbide products increased by approximately 31% YoY from January to May 2025, with a significant growth rate in the second quarter. The total export volume of drill bit and drilling machine products increased by approximately 22.3% YoY.

Additionally, the demand for tungsten in the military sector has grown significantly in 2025. Geopolitical conflicts overseas, coupled with global military upgrades (such as Europe's "Sky Shield Plan"), have made tungsten irreplaceable in military products such as missile components and cutting tools. Continuous overseas military disputes have, to a certain extent, increased the demand growth for tungsten metal materials.

In summary, the main driving factors for the tungsten market to fluctuate at highs are the tightening supply-demand relationship in the ore sector, coupled with low global tungsten inventory, and the global supply tightening of tungsten due to China's export controls on tungsten products. Entering the second half of June, the tungsten market entered a tug-of-war between longs and shorts. Prices of raw materials such as ore fluctuated at highs, while the slow increase in prices in the powder sector and the tungsten chemical products industry led to poor corporate profitability, highlighting the contradiction and restraining price increases in the industry. In the medium and long-term, it is likely that the production and grade of domestic tungsten concentrate will decline, and overseas supply growth will be slow, resulting in a continued tight supply situation in the ore sector. Combined with the current situation of low industry inventory, driven by the growth in end-use demand, there will still be a need for restocking in the future market. The profit distribution in the tungsten industry chain may be reshaped, thereby supporting prices in the entire industry chain to hover at highs.

》View SMM tungsten and molybdenum product quotes, data, and market analysis

》Click to view SMM molybdenum spot quotes

》Subscribe to view historical price trends of SMM metal spot prices